Symmetry Principles, Maximum Entropy and Robust Portfolios

(Published by JP Bouchaud | November 2024)

Markowitz’ celebrated optimal portfolio theory generally fails to deliver out-of-sample diversification. In a note published in October 2016, Raphaël Benichou and other CFM researchers proposed a new portfolio construction strategy based on symmetry principles only.

This allowed us to define “Eigenrisk Parity” portfolios that achieve equal realized risk on all the principal components of the covariance matrix. This equal risk property in fact holds true for any other definition of uncorrelated factors. The resulting portfolio weights w* read:

w* = C^{-1/2} Q^{-1/2} g,

where C is the covariance matrix of the assets, and Q the covariance matrix of the predictors g.

When Q=C, i.e. when the correlation structure of predictors is the same as that of the assets in the investable universe, one recovers the usual Markowitz formula. As is well known, such a portfolio over-allocates in the directions associated to the small eigenvalues of C, i.e. the `low-risk’ directions.

Conversely, when w*=1/N (equi-allocation across assets), the portfolio over-allocates in the directions associated to the large eigenvalues of C, i.e. the `high-risk’ directions.

The “Agnostic Risk Parity” (ARP) portfolio we proposed in 2016 corresponds to Q=I, i.e. refusing to take seriously any correlations across predictors. Our argument was that this is a way to minimize unknown-unknown risks generated by over-optimistic hedging of the different bets. It corresponds to an equi-risk allocation over all directions, low-risk and high-risk.

In a way, Agnostic Risk Parity is the correct implementation of the maximum entropy principle for portfolio construction, once symmetries have been accounted for -- see our paper

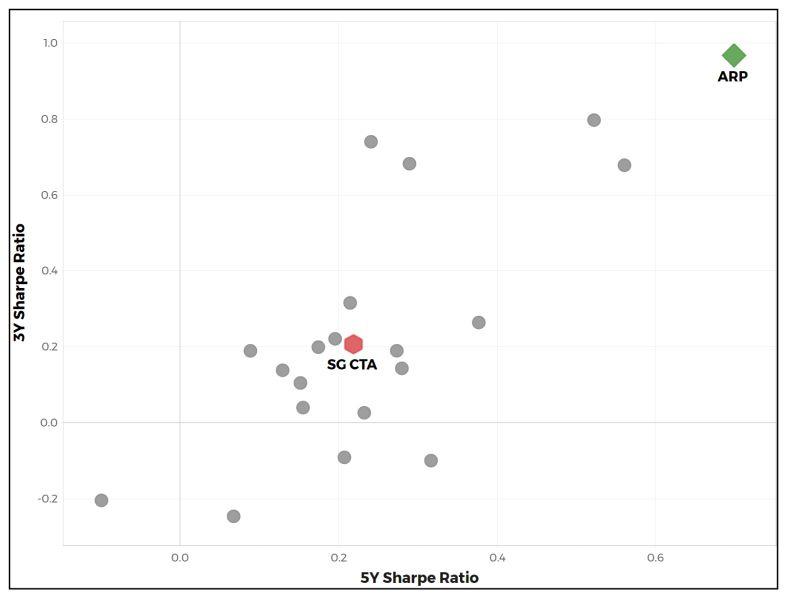

Is all this a figment of theorists’ imagination, or can this be used in practice? Using backtests, we showed at the time that the ARP portfolio could potentially improve the performance of trend following strategies on futures by 20% in the period 1998 – 2016 (see Fig. 2 of our paper).

More convincingly, such a portfolio construction has been used in real trading since June 2016. The result is shown in the figure below. Our ARP trend-following strategy (green square) shows higher 3-year and 5-year Sharpe ratios (calculated over a period ending in August 2024) than the SG CTA index (red circle) and its components (grey circles, where we were able to retrieve their unaudited performance from available sources).

Portfolio construction does matter! Symmetry principles and agnostic arguments allow one to extract significant value from relatively standard technical signals.