Fat Tails and Diversification

(Published by JP Bouchaud | January 2023)

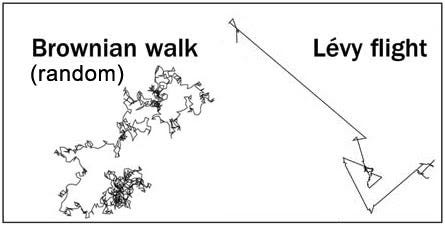

I have been fascinated by non Gaussian, fat-tailed distributions ever since I began doing science. My very first paper in 1984 (with P. Le Doussal) was on the so-called “Sinai billiard”, i.e. a point particle bouncing off an infinite, regular array of perfectly elastic, circular obstacles. As proven by Y. Sinai, this is an ergodic system, but with a particular property: the particle undergoes super-diffusion, i.e. its mean square displacement grows faster than linearly with time.

The reason is that the particle manages to occasionally find itself on trajectories that travel very far before hitting the next obstacle. In fact, the distribution of distances before the next collision has a diverging variance. The resulting motion is a "Lévy flight”, not a Brownian motion (see figure below).

Perhaps by accident or perhaps because I have a special penchant for these types of systems, my subsequent work in statistical physics gyrated around fat-tailed distributions, on the shoulder of the great Benoît B. Mandelbrot. (Q: Do you know what the second B. stands for? A: Benoît B. Mandelbrot…). Fat-tailed distributions arise naturally in many physical systems (avalanches, earthquakes, glassy dynamics, etc.) but also of course in economic and financial systems (wealth, firm sizes, price returns, etc.).

This is actually what lured me into quantitative finance: the total disconnect between the Gaussian world of Black & Scholes, where perfect hedging is possible, and the fat-tailed world of financial markets that makes perfect hedging impossible and Black & Scholes a very bad theory to account for option smiles. These ideas led me to join CFM and are at the core of our volatility arbitrage program since 2005.

One of the defining feature of fat-tailed random variables is the dominance of rare, but large events. Draw N independent, identically distributed random variables and compare the probability P that the largest of these N random variables exceeds some large number K, to the probability Q that the *whole sum* of the same N random variables exceeds K.

Fat-tailed distributions are such that P and Q are of the same order of magnitude when K becomes large, that is: one catastrophic variable is enough to explain large deviations of the whole sum. For thin-tailed distributions, on the other hand, P is much smaller than Q, i.e. many variables have to “conspire” to build up a large sum.

This discussion is very relevant in the context of portfolio returns. Are large losses due to a single asset (or a single strategy) going haywire or are they due to all assets accidentally conspiring to create a large negative return? Good risk control clearly means the latter.

There are many good books on these topics. I would particularly recommend the recent “Fundamentals of Heavy Tails” by J. Nair, A. Wierman & B. Zwart

#financialmarkets #crashes #Levy #options

Can you explain why "Good risk control clearly means the latter"?